Algorithm

Consider the linear regression with samples  satisfying:

satisfying:

Here  is an unknown parameter vector relating the covariates

is an unknown parameter vector relating the covariates  to the response

to the response  , and

, and  are noise terms. ‘‘The covariates are potentially collected adaptively, and so can be correlated to prior covariates

are noise terms. ‘‘The covariates are potentially collected adaptively, and so can be correlated to prior covariates  .’’

.’’

Goal: We aim at ex post statistical inference on individual model parameters  , in terms of frequentist p-value and confidence interval.

, in terms of frequentist p-value and confidence interval.

Method

Below we provide a brief explanation of the online debiasing method. For more details and scissions, we refer to our paper.

Denote by  the Lasso estimator

the Lasso estimator

The online debased estimator  takes the form

takes the form

The term ‘online’ comes from the crucial constraint of predictability imposed on the sequence: there exists a filtration  so that, (1) are adapted to

so that, (1) are adapted to  and is independent of

and is independent of  for

for  . We assume that the sequences

. We assume that the sequences  and

and  are predictable with respect to

are predictable with respect to  .

.

How to choose decorrelating matrices?

We focus on times series as an important application of adaptively collected data and consider a vector autoregression (VAR) model for time series. By a proper change of variables, a Var(d) model can be represented as the linear regression with  parameters and

parameters and  sample size where

sample size where  is the time horizon where we observe the times series, and

is the time horizon where we observe the times series, and  is the lag. Our primary interest is in high-dimensional Var(d) model, where the number of model parameters exceeds the sample size .

is the lag. Our primary interest is in high-dimensional Var(d) model, where the number of model parameters exceeds the sample size .

The proposed online debiasing provides valid statistical significance measures for the model parameters (the time invariant matrices in the Var(d) model).

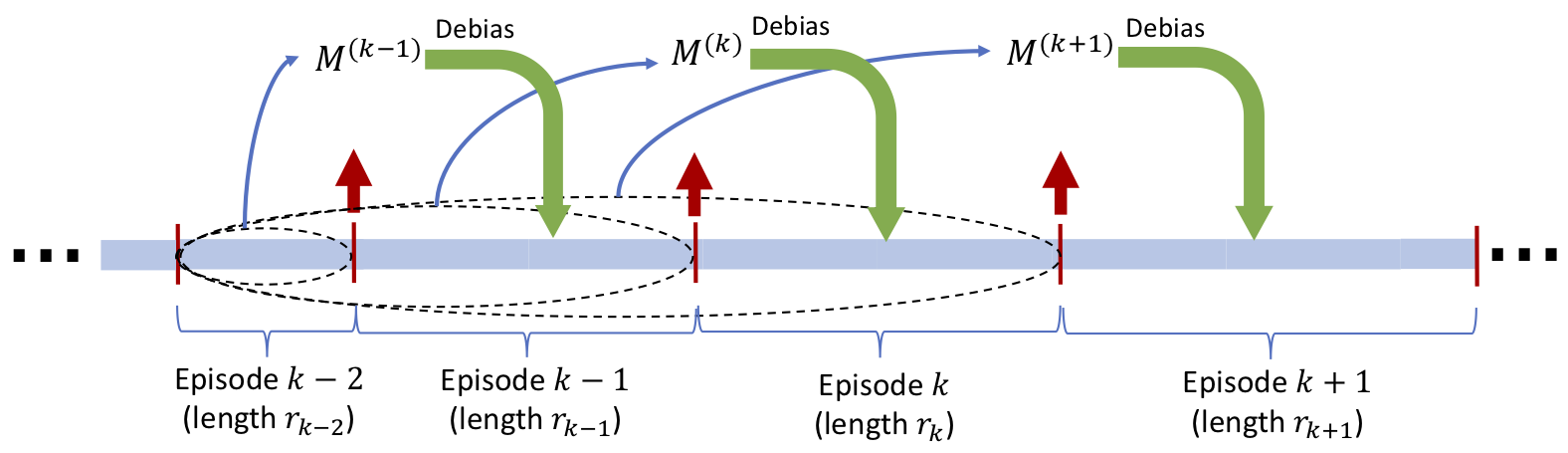

To construct decorrelating matrices  that satisfy the predictability condition, we proceed as follows:

that satisfy the predictability condition, we proceed as follows:

For given positive integer numbers

that add up to

that add up to  , we partition the time horizon into episodes

, we partition the time horizon into episodes  , with

, with  of length

of length  and let

and let  be the sample covariance of features in the first

be the sample covariance of features in the first  episodes.

episodes.

|

At the beginning of each episode

, we calculate a decorrelating matrix  using the previous data points and use that matrix to debias the sample coming in the current episode, that is to say

using the previous data points and use that matrix to debias the sample coming in the current episode, that is to say  for

for  . The details of this step are summarized in the box below.

. The details of this step are summarized in the box below.

1. For  do

Construct

do

Construct  by solving the following optimization:

by solving the following optimization:

With  the standard basis element with one at the

the standard basis element with one at the  -th position and zero everywhere else.

-th position and zero everywhere else.

2. Set  . In words, stack the constructed vectors

. In words, stack the constructed vectors  as rows of .

as rows of .

Our analysis in the paper suggests the choice of episode lengths  . The code can take the parameter

. The code can take the parameter  as an input.

as an input.